When you try to move money between a crypto exchange and a bank in Cyprus, you might hit a wall. It’s not because crypto is banned. It’s because the rules changed-dramatically-and banks are now forced to treat crypto transactions like high-risk wire transfers. If you’re running a crypto business or just holding digital assets in Cyprus, understanding these restrictions isn’t optional. It’s the difference between smooth operations and frozen accounts.

Why Cyprus Changed the Rules

Cyprus used to be one of the friendliest places in Europe for crypto businesses. Low taxes, English-speaking staff, and a streamlined registration process drew companies from all over. But in 2023, everything shifted. The EU’s Markets in Crypto-Assets (MiCA) regulation came into force, and Cyprus had to align its laws. This wasn’t a local decision-it was a legal requirement. Suddenly, every bank, payment provider, and crypto exchange had to follow the same strict rules as banks handling wire transfers. The trigger? Money laundering risks. The European Central Bank and the Financial Action Task Force (FATF) pushed member states to close loopholes. Cyprus responded by passing the Prevention and Suppression of Money Laundering from Illegal Activities (Amendment) (No. 2) Law of 2025. This law redefined crypto-asset service providers (CASPs) as financial institutions. That meant banks had to treat them like any other high-risk client-subject to full due diligence, real-time monitoring, and mandatory reporting.The Travel Rule: The Biggest Hurdle

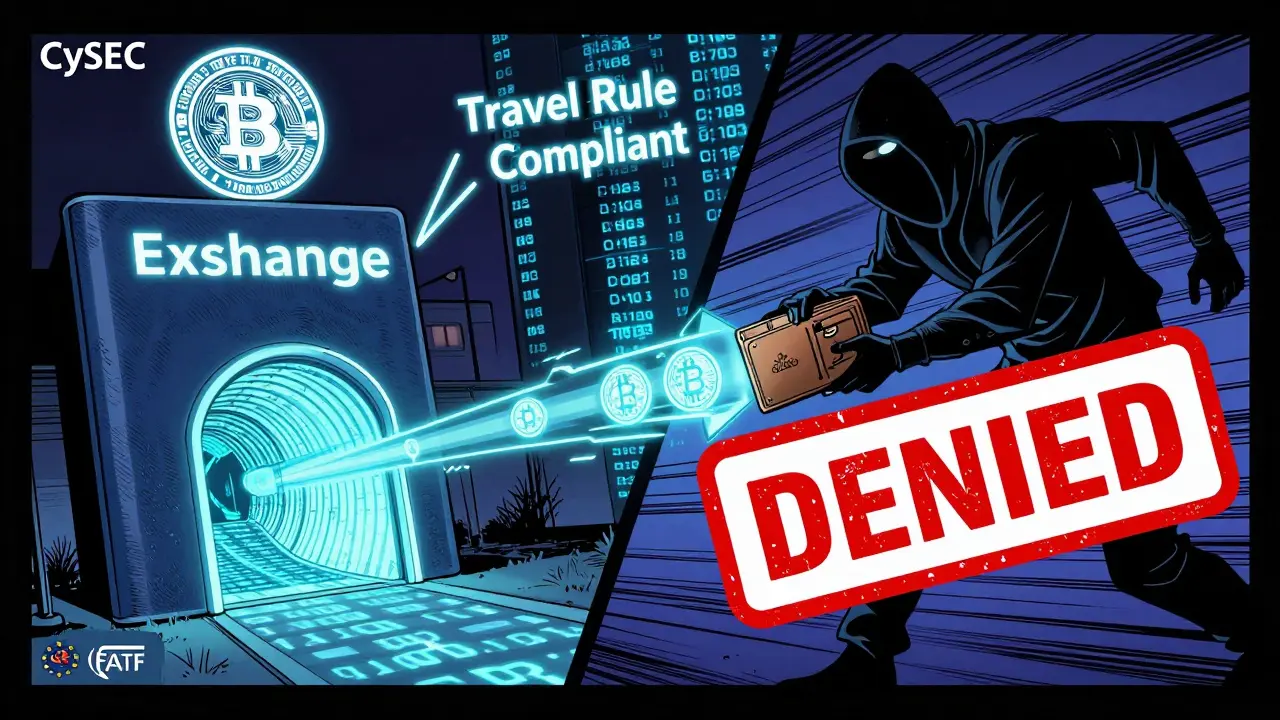

The most impactful change? The Travel Rule. Under EU Regulation (EU) 2023/1113, any crypto transaction over €1,000 must carry full sender and receiver data. That includes names, addresses, ID numbers, and account details. This data must travel with the funds-just like a bank wire. For banks, this isn’t a suggestion. It’s mandatory. If a crypto transfer comes in without this data, the bank must block it. No exceptions. Even if the sender is a known customer, if the recipient is a self-hosted wallet (like a personal MetaMask), the bank has to stop the transaction until identity verification is complete. According to AGP Law’s September 2025 analysis, this single rule has caused a 40% spike in declined transactions across Cypriot banks. Many users don’t realize their wallet doesn’t have the right data attached. And banks aren’t allowed to guess or assume-they have to verify everything.Who’s in Charge? CySEC and the Central Bank

Cyprus didn’t create one regulator. It split oversight. The Cyprus Securities and Exchange Commission (CySEC) is the primary authority for authorizing and supervising crypto-asset service providers (CASPs). Any exchange, custodian, or trading platform operating in Cyprus must register with CySEC, prove they have enough capital, and show they have AML procedures in place. As of Q2 2025, CySEC had registered 87 CASPs. Meanwhile, the Central Bank of Cyprus (CBC) controls how traditional banks interact with crypto. The CBC doesn’t regulate crypto itself-it regulates the banks that touch it. That’s why even if a crypto company is fully licensed, a bank can still refuse to open an account. The CBC requires banks to:- Perform enhanced due diligence on all CASPs they work with

- Verify the identity of counterparties in every crypto transaction

- Screen all transfers against EU and UN sanctions lists

- Keep detailed audit trails for at least five years

Real-World Impact: What Businesses Are Facing

A Q2 2025 survey by the Cyprus Blockchain Association found that 68% of crypto businesses struggled to open or keep a bank account. Some lost accounts overnight when their bank reviewed their transaction history and flagged too many crypto-related transfers. Here’s what’s happening on the ground:- Transaction delays: Real-time beneficiary verification adds 15-20 seconds per transaction. For high-volume exchanges, that’s hours of backlog.

- Account closures: Banks are terminating relationships with CASPs that don’t have full CySEC registration or have high-risk clients.

- Increased costs: Compliance teams now need dedicated staff to handle AML filings, sanctions checks, and audit logs. Small firms are spending 20-30% of revenue just on compliance.

What You Can’t Do Anymore

Here are the three biggest restrictions that caught people off guard:- No direct deposits from self-hosted wallets: If you try to send ETH from your personal wallet to a Cypriot bank account, the bank will likely reject it unless you can prove the wallet belongs to you and provide full KYC data.

- No anonymous crypto-to-fiat swaps: Even if you use a licensed exchange, if you’re not fully verified, you can’t cash out. Exchanges now lock withdrawals until ID, proof of address, and source of funds are confirmed.

- No bulk crypto payments: Businesses that used crypto for payroll or vendor payments now need to convert to euros first. Banks won’t accept deposits from multiple crypto sources unless each one is individually verified.

What’s Still Allowed

Despite the restrictions, Cyprus still has advantages:- No capital gains tax: If you sell Bitcoin or Ethereum for profit, you pay zero tax. This hasn’t changed.

- Legal registration: You can still register a crypto business with CySEC. Over 87 have done it.

- EU market access: Once registered, your business can operate across the EU under MiCA’s passporting rules.

- Instant euro payments: By 2027, all banks must offer instant SEPA transfers. This makes converting crypto to euros faster than ever-once the money clears.

How to Stay Compliant

If you’re a business in Cyprus, here’s what to do right now:- Register with CySEC if you’re handling crypto assets.

- Implement a full AML/CFT policy with staff training and internal audits.

- Use only CASPs that are verified by CySEC for all transactions.

- Never send crypto to unverified wallets-especially self-hosted ones.

- Keep records of every transaction, including wallet addresses and verification logs.

- Work with a compliance consultant familiar with MiCA and Cyprus’s 2025 amendments.

The Future: Tighter Controls, Not Less

Cyprus isn’t backing down. In fact, it’s doubling down. The National Sanctions Unit launched in late 2025 gives the government centralized power to freeze crypto assets linked to sanctioned individuals. Banks now have real-time access to this database. By 2027, experts predict 95% of crypto transactions in Cyprus will go through registered CASPs. That’s up from 78% in early 2025. The goal isn’t to kill crypto-it’s to make every transaction traceable. The government sees this as a way to attract legitimate businesses while pushing out bad actors. The message is clear: You can still do crypto in Cyprus. But you have to do it the right way. No shortcuts. No gray zones. Just full transparency.Can I still use Bitcoin in Cyprus?

Yes, you can hold, buy, and sell Bitcoin in Cyprus. But you can’t use it as payment for goods or services unless the business voluntarily accepts it. Banks won’t process direct Bitcoin deposits. You must convert Bitcoin to euros through a licensed exchange first, then deposit the euros into your bank account.

Do I need to pay taxes on crypto profits in Cyprus?

No, Cyprus does not charge capital gains tax on cryptocurrency sales or exchanges. This remains unchanged as of 2026. However, if you earn income from crypto (like staking rewards or mining), it may be subject to income tax. Always consult a tax advisor for personal situations.

Can a Cypriot bank refuse to bank my crypto company?

Yes. Even if your company is fully registered with CySEC, a bank can still refuse to open or keep an account. Banks are not required to work with crypto businesses. They assess risk individually and often avoid crypto exposure due to compliance burdens and regulatory scrutiny.

What happens if I send crypto to a wallet without KYC?

If you send crypto from a licensed exchange to a self-hosted wallet without verified identity, the transaction may be flagged or blocked under the Travel Rule. If you later try to cash out from that wallet back into a Cypriot bank, the bank will likely reject the deposit unless you can prove ownership and provide full KYC documentation. This creates a major bottleneck for individuals using personal wallets.

Is Cyprus still a good place to start a crypto business?

Yes-if you’re prepared for compliance. Cyprus offers EU market access, no capital gains tax, and a clear regulatory path through CySEC. But the cost and complexity of compliance have increased significantly since 2025. Businesses that succeed now are those that treat compliance as core to their operations, not an afterthought.

If you’re planning to move crypto in or out of Cyprus, remember: the rules aren’t going away. They’re getting stricter. Your best move? Play by the book. Use licensed services. Keep records. And never assume a bank will accept crypto without proof.

Angela Henderson

February 19, 2026 AT 09:21So basically, if I want to move my crypto to my bank account in Cyprus, I now need to fill out a passport application for my wallet? I mean, I get that they’re trying to stop bad actors, but this feels like locking the front door and then putting a 10-foot steel gate behind it. I’ve got a friend who runs a small NFT art studio there, and she’s been stuck for months trying to pay her printer. Every time she sends ETH, the bank freezes it. She had to hire a compliance consultant just to explain what a wallet address is. It’s not even about money anymore-it’s about dignity. Why does the system treat honest people like criminals? I just wish there was a middle ground where we didn’t have to jump through 17 hoops just to move our own assets.

And don’t even get me started on the ‘Travel Rule.’ It’s like the EU said, ‘Hey, let’s make crypto behave like a 1980s bank wire.’ But crypto was supposed to be the future, right? Not a glorified SWIFT system with more paperwork.

JJ White

February 20, 2026 AT 15:33Oh, wonderful. Another EU regulation that turns innovation into a bureaucratic nightmare. They didn’t ‘align’ with MiCA-they surrendered. Cyprus used to be the wild west of crypto in Europe, and now it’s just another beige office with fluorescent lighting and a guy in a suit asking for your birth certificate before he’ll let you send 0.001 BTC. This isn’t regulation-it’s surrender. And the worst part? The banks are the ones who *chose* to make this hellish. They could’ve worked with CySEC to build a smarter system. Instead, they went full panic mode. ‘We don’t know what crypto is, so we’ll block everything.’ Brilliant. Absolutely brilliant. Now the only people who can still do business are the ones with lawyers on retainer. Congrats, Europe. You’ve won. Crypto is now just another form of corporate tax evasion.

Alan Enfield

February 21, 2026 AT 19:47From a compliance standpoint, this is actually pretty logical. The Travel Rule isn’t unique to Cyprus-it’s an EU-wide standard under AMLD6 and MiCA. The real issue is implementation. Most small CASPs don’t have the infrastructure to handle real-time KYC for self-hosted wallets. The tech exists, but it’s expensive. You need blockchain analytics platforms, identity verification APIs, and audit trails. For a startup, that’s 30% of your burn rate. The banks aren’t being unreasonable-they’re just following the law. The problem is the gap between regulation and operational reality. If CySEC offered a sandbox for testing interoperable wallet solutions, we might actually solve this instead of just blocking everything. But no one’s talking about that. Everyone’s just screaming about ‘freedom’ or ‘authoritarianism.’

Jennifer Riddalls

February 23, 2026 AT 07:04Just wanted to say I really appreciate how clear this post is. I’m new to crypto and was terrified to even try moving funds from my exchange to my local bank. Now I get why it’s so strict. It’s not that they hate crypto-it’s that they’ve seen too many people get burned by scams and then blame the system. I’ve got my KYC done, I’m using a CySEC-registered exchange, and I convert everything to euros before depositing. It’s slower, yeah, but it’s safe. And honestly? That’s worth it. I’d rather wait 2 days than lose everything because I thought ‘I’ll just send it directly.’ You don’t need to be a genius to stay out of trouble here. Just be smart. And patient. And maybe keep receipts.

Also, no capital gains tax? Yes please. That’s the real win.

Kyle Tully

February 23, 2026 AT 21:25Let me get this straight. You can’t send crypto from your own wallet to your own bank account unless you prove you own the wallet? So if I bought ETH on Coinbase and then sent it to my MetaMask, I’m now a criminal because I tried to move my own money? That’s not regulation-that’s identity theft. The system is designed to make you feel like your assets aren’t yours anymore. They’re owned by the state. And if you don’t jump through their hoops? Too bad. You’re just a rogue actor. This isn’t about money laundering. It’s about control. They don’t trust you. And they don’t want you to trust yourself. That’s the real story here. Crypto was supposed to be about sovereignty. Now it’s about submission.

yogesh negi

February 24, 2026 AT 12:52Bro, this is actually very well explained. I live in India and we have our own crypto chaos-banks blocking UPI transfers, tax confusion, and random freezes. But seeing how Cyprus handled it? Honestly, it’s more organized than what we have. At least here, there’s a clear regulator (CySEC), clear rules, and even a timeline. In India, we’re just waiting for some minister to tweet ‘crypto is bad’ and then everything gets banned overnight. Here, they’re building a system. Yes, it’s strict. Yes, it’s annoying. But at least it’s predictable. I’ve got a friend who started a crypto payroll company in Cyprus last year. He’s got 12 employees now. All EU-compliant. All paid in euros. All happy. The system works if you respect it. Don’t fight the system. Learn it. Use it. And then thrive.

george chehwane

February 24, 2026 AT 21:06The Travel Rule isn’t about anti-money laundering-it’s about surveillance capitalism repackaged as financial regulation. They don’t care if you’re laundering money. They care that you’re transacting outside their control. The blockchain is the last unmonitored financial layer left in the world. And now they’re stitching it into the banking grid like a prisoner being fitted for shackles. This isn’t compliance. It’s assimilation. The EU didn’t ‘align’ with MiCA-they weaponized it. The moment crypto became traceable, it lost its soul. Now it’s just another payment rail with extra paperwork. The real innovation died the moment the first bank demanded a KYC form for a wallet address. You can’t regulate decentralization. You can only crush it. And that’s exactly what they’re doing.

Jenn Estes

February 25, 2026 AT 04:17People are acting like this is some new horror story. Newsflash: This has been coming since 2018. The FATF warned everyone. The ECB screamed. The EU passed the rules. And yet somehow, everyone acted like crypto was exempt from reality. You thought you could hide behind ‘decentralization’ while still using banks? That’s not rebellion. That’s delusion. The banks didn’t ‘change’-they finally enforced what they’ve been legally required to do for years. If you didn’t prepare for this, that’s on you. Not the system. Not the regulators. You. Stop crying about ‘freedom’ when you refused to do the work. Compliance isn’t optional. It’s the price of entry. And you didn’t pay.

Jeremy Fisher

February 25, 2026 AT 13:08I’ve lived in Cyprus for 12 years. Used to work in finance before I switched to crypto. I remember when the first crypto business opened here-2017. Everyone was excited. No taxes, English everywhere, beaches, sunshine. Now? The same people who cheered are the ones complaining about the rules. But here’s the thing: Cyprus didn’t change. The world changed. The EU got serious. The U.S. started cracking down. Crypto went from ‘cool side hustle’ to ‘global financial threat.’ And suddenly, everyone who thought they could ride the wave without getting wet got soaked. The truth? Cyprus is still one of the best places to do this. You just have to play by the rules now. No more shortcuts. No more ‘I’m just a guy with a wallet.’ If you want to operate here, you need structure. And structure costs. But it’s worth it. I’ve seen businesses fail because they thought they could wing it. The ones that survived? They built teams. They hired lawyers. They kept records. And now? They’re expanding across the EU. It’s not glamorous. But it works.

sruthi magesh

February 26, 2026 AT 14:55EU? More like EUnuch. They’re scared of crypto because it’s faster than their paper-based bureaucracy. They want to control everything. But you can’t control what you don’t understand. Crypto is the future. And this? This is the last gasp of a dying financial system. India doesn’t need this nonsense. We’re building our own blockchain. We don’t need your KYC forms. We don’t need your ‘Travel Rule.’ We have our own rules. And we’re not waiting for Brussels to decide if we can send money. You’re not regulating crypto. You’re just trying to bury it under paperwork. And guess what? It’s not working. The tech is too smart. The people are too hungry. The revolution isn’t coming. It’s already here. And you’re just the old man yelling at the clouds.

Nova Meristiana

February 27, 2026 AT 17:47Ugh. Another ‘educational’ post that’s just a glorified press release from CySEC. Look, I get it. You want to sound like you’re ‘helping.’ But this isn’t transparency-it’s propaganda. They’re not ‘making crypto traceable.’ They’re making it taxable. And guess who gets to audit every single transaction? The government. And guess who pays for the compliance? You. The ‘no capital gains tax’ is just a lure. Wait until they introduce a ‘crypto transaction levy’ under ‘administrative fees.’ It’s already happening in Luxembourg. They’ll call it ‘stability funding.’ It’s not regulation. It’s taxation by stealth. And the fact that you’re all drinking the Kool-Aid? Classic. You’re being sold a luxury prison and calling it a paradise.

Nicole Stewart

March 1, 2026 AT 11:46So. The rules changed. Banks won’t accept crypto. Big deal. I’m not surprised. Crypto was always a gamble. Now it’s a regulated gamble. You want to play? Fine. Pay the price. Don’t act like this is some injustice. You knew the risks. You chose this. Now deal with it. Stop whining. It’s not that hard. Use an exchange. Convert. Deposit. Done. No one forced you to hold crypto in a wallet. You did. So stop pretending you’re a victim. This isn’t oppression. It’s consequence.

kieron reid

March 1, 2026 AT 19:31Let’s be real. The entire premise of this post is flawed. The ‘restrictions’ aren’t new. They’ve been in place since 2023. The real story? No one told the average crypto user. They thought they could keep using their wallet like a bank account. They didn’t read the fine print. They assumed ‘EU regulation’ meant ‘easy access.’ It doesn’t. It means ‘strict oversight.’ The problem isn’t Cyprus. It’s the crypto community’s collective refusal to acknowledge that this isn’t a game anymore. It’s a financial system. And systems have rules. You ignored them. Now you’re mad when they’re enforced. Wake up.

Avantika Mann

March 2, 2026 AT 10:47Hey everyone, I just wanted to say this is such a helpful breakdown. I’m just starting out with crypto and was so confused about why my bank kept rejecting transfers. Now I get it-it’s not personal. It’s policy. I’ve been using a CySEC-registered exchange, and honestly, the process is smoother than I expected. I just make sure my ID and proof of address are up to date. Took me 20 minutes. And now I can cash out without stress. I know it feels restrictive, but if you take the time to do it right, it’s not that bad. And honestly? It’s kind of reassuring to know there’s a system in place. It means my money is safer. I’m not saying it’s perfect. But I’m saying: try to work with it, not against it. You’ll thank yourself later.

Nikki Howard

March 3, 2026 AT 00:26While the regulatory framework is robust, I must point out a critical oversight: the post does not address the impact on SMEs with under €500k annual turnover. These businesses cannot afford the €20k/year compliance overhead. The current system favors institutional players and actively disincentivizes grassroots adoption. Furthermore, the Central Bank’s refusal to define ‘self-hosted wallet’ legally creates ambiguity. Is a Ledger device a ‘wallet’? Is a paper wallet? The lack of legal clarity renders the Travel Rule unenforceable in practice. This is not regulation. It is regulatory capture disguised as public safety.

Tarun Krishnakumar

March 4, 2026 AT 15:34Let me tell you what’s really going on. This isn’t about money laundering. It’s about the banks losing control. Crypto was supposed to be peer-to-peer. But now? Every transaction has to be logged, tracked, and approved by a central authority. Who benefits? The same people who run the old banking system. The ‘Travel Rule’? It’s not about safety. It’s about surveillance. They don’t want you to have anonymous money. They want you to be tracked. And the moment you use a self-hosted wallet? They panic. Why? Because they can’t see it. They can’t tax it. They can’t control it. So they made it illegal to use without permission. This isn’t regulation. It’s a power grab. And the fact that everyone is celebrating this as ‘compliance’? That’s the real scam. You’re being sold a cage and told it’s a palace.

jennifer jean

March 4, 2026 AT 15:56Wow, this is so helpful 😊 I was so confused before, but now I get it. I’m just a regular person trying to hold some ETH, and I didn’t realize how much the banks had to do. I’m going to use a licensed exchange now and convert to euros. Feels way safer. And no capital gains tax? That’s a win 🙌 Thanks for breaking it down so clearly!

Sasha Wynnters

March 6, 2026 AT 13:55They didn’t ban crypto. They baptized it. Turned the wild, decentralized, anarchic dream of peer-to-peer value into a regulated, audited, compliance-laden corporate entity. The blockchain didn’t die. It got a suit. And now it’s in a conference room, filling out Form 7B-23 with a fountain pen, while the old guard sips espresso and nods approvingly. This isn’t evolution. It’s domestication. Crypto didn’t lose its soul-it was surgically removed during a routine audit. The system didn’t adapt. It absorbed. And now, every transaction carries the scent of bureaucracy. You can still hold Bitcoin. But you can’t feel it anymore. You can’t touch it. You can’t trust it. You can only document it. And that? That’s the real tragedy. Not the rules. The surrender.