Imagine trying to buy coffee in Berlin or pay rent in Paris using your favorite digital currency, only to find out the platform you use is no longer allowed to trade it. That is exactly what happened across the European Union when the Markets in Crypto-Assets (MiCA) regulation fully enforced its strict rules on stablecoins. If you hold tokens like Tether (USDT), this isn't just bureaucratic noise; it is a fundamental shift in how you can access, trade, and use your assets within Europe.

The era of the wild west in European crypto markets ended decisively in early 2025. Under MiCA, stablecoins are no longer treated as generic tech experiments. They are now classified into two specific legal buckets: Asset-Referenced Tokens (ARTs) and E-Money Tokens (EMTs). This classification dictates everything from where reserves must be held to who gets to issue them. For users, the most immediate impact was the forced delisting of non-compliant tokens from major exchanges. Let’s break down what this means for your portfolio, why USDT faces such hurdles, and how the landscape looks in mid-2026.

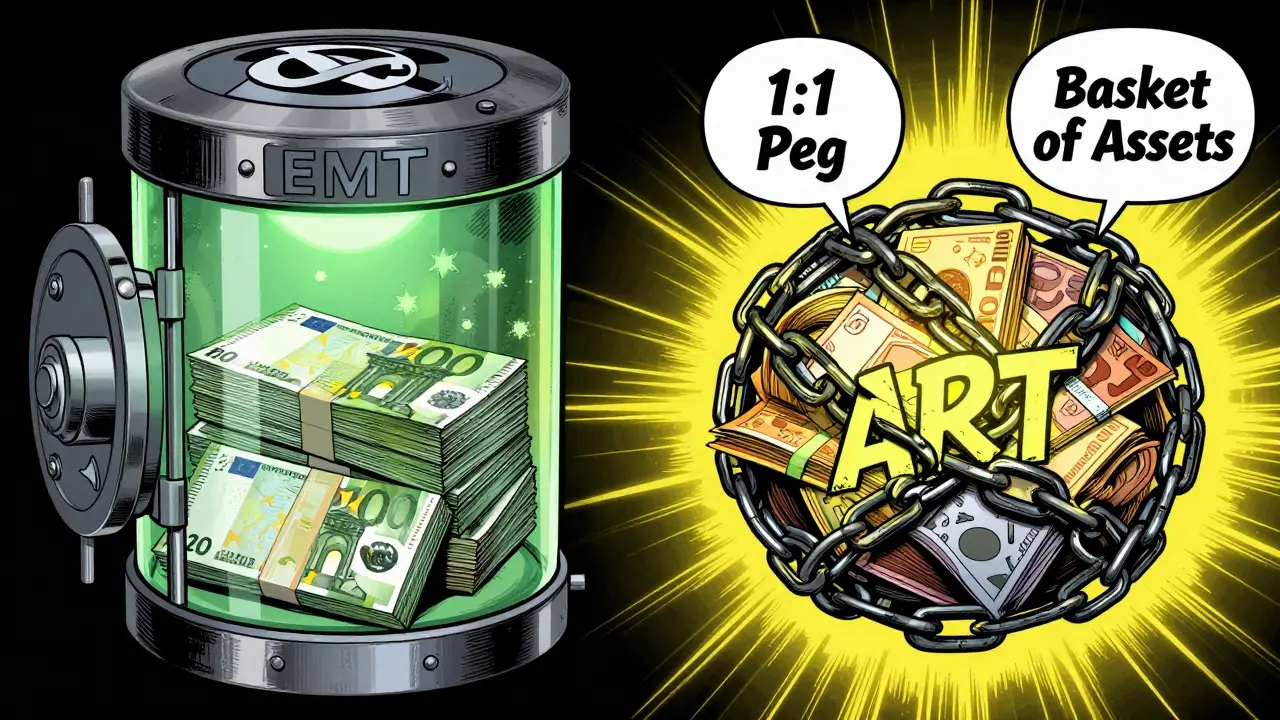

The Two Buckets: Understanding EMTs and ARTs

To understand why some coins survived and others got kicked off trading platforms, you first need to know how MiCA categorizes them. The regulation does not see all stablecoins as equal. It splits them based on their backing mechanism and complexity.

E-Money Tokens (EMTs) are the simpler category. These are tokens pegged 1:1 to a single fiat currency, like the Euro or the US Dollar. Think of them as digital cash. Because they mimic traditional electronic money, the rules for them are strict but straightforward. Issuers must hold reserves in highly liquid, low-risk assets-essentially cash or government bonds-and these reserves must be kept separate from the issuer’s own operational funds to protect against bankruptcy. Crucially, holders have the right to redeem these tokens at par value directly with the issuer.

Asset-Referenced Tokens (ARTs) are more complex. These tokens attempt to maintain stability by referencing a basket of currencies or other assets, rather than just one. Because they involve more complex hedging strategies and carry higher systemic risk, MiCA treats them almost like financial securities. Issuing an ART requires authorization from national competent authorities and involves significantly heavier capital requirements and transparency obligations.

This distinction matters because most popular global stablecoins, including USDT, do not neatly fit the compliant EMT mold under current structures. While USDT claims to be backed by cash and equivalents, its reserve composition and lack of direct par-value redemption mechanisms for retail users in the EU triggered non-compliance flags under MiCA’s stringent definitions.

Why USDT Faces Major Hurdles in the EU

You might wonder why a token as ubiquitous as Tether (USDT) is facing such headwinds. The issue boils down to transparency and reserve structure. MiCA demands that issuers provide real-time proof of reserves and ensure those reserves are held in bankruptcy-protected structures within the jurisdiction or under strict international agreements.

Historically, Tether’s reserve disclosures have been opaque enough to raise eyebrows among regulators. The Bank for International Settlements (BIS) highlighted in its 2025 Annual Economic Report that many major stablecoins, including USDT, had experienced "substantial deviations from par" during market stress. This fragility is precisely what MiCA aims to eliminate. By requiring one-for-one reserves in high-quality liquid assets, the EU ensures that if a bank holding those reserves fails, your stablecoin doesn’t vanish.

Furthermore, MiCA grants users the right to redeem their tokens at face value. If you hold €1,000 worth of a compliant EMT, you should be able to get €1,000 back in euros, period. USDT has historically made this process difficult for individual retail users, often restricting redemptions to institutional clients. Without offering this direct redemption pathway to all holders, USDT cannot achieve full compliance status as an EMT in the EU.

| Feature | MiCA Compliant (EMT) | Non-Compliant (e.g., Pre-MiCA USDT) |

|---|---|---|

| Reserve Backing | 1:1 Cash/Gov Bonds, segregated accounts | Mixed assets, commercial paper (historically) |

| Redemption Right | Guaranteed at par for all holders | Limited or institutional-only |

| Transparency | Real-time reserve attestation required | Quarterly or semi-annual attestations |

| Trading Status in EU | Fully tradable on licensed CASPs | Delisted from trading pairs as of Q1 2025 |

| Issuer Liability | Strict liability for reserve shortfalls | Limited recourse for retail users |

The Role of CASPs: Your Exchange’s New Job

If you trade crypto in Europe, you interact with Crypto-Asset Service Providers (CASPs). These are your exchanges, wallet providers, and trading platforms. Under MiCA, their role changed dramatically. They are no longer just passive intermediaries; they are active enforcers of regulatory compliance.

By the end of January 2025, ESMA mandated that all licensed CASPs in the EU delist non-compliant stablecoins from their trading pairs. This means you can no longer buy or sell USDT for Euros or Bitcoin on major European platforms like Kraken, Bitstamp, or Coinbase EU. However, the regulation did not ban ownership entirely. You can still hold USDT in your private wallet, and CASPs must allow you to transfer it in and out for custody purposes. But you cannot easily convert it into other assets through regulated channels.

This creates a liquidity trap for holders. If you want to exit your USDT position, you might have to rely on peer-to-peer (P2P) markets or decentralized exchanges (DEXs) that operate in a gray area, which often come with higher slippage and security risks. For institutions, this forced a rapid portfolio rebalancing toward compliant alternatives.

The Rise of European Alternatives

Regulations often kill innovation, but in this case, they sparked a race to build homegrown solutions. Recognizing that relying on US-dominated stablecoins poses a strategic risk to Europe’s monetary sovereignty, nine major European banks formed a consortium. This group includes giants like ING, UniCredit, and Danske Bank.

Their goal? To launch a Euro-denominated stablecoin that is fully compliant with MiCA from day one. Established in the Netherlands and seeking supervision from the Dutch Central Bank, this project aims to offer a "real European alternative." Expected to launch in the second half of 2026, this token will likely serve as the backbone for instant cross-border payments within the EU, leveraging blockchain’s 24/7 settlement capabilities without the regulatory friction of foreign tokens.

For everyday users, this means we may soon see seamless integration of this new euro-stablecoin into banking apps and payment processors. Imagine paying for groceries with a token that settles instantly, costs fractions of a cent, and is guaranteed by the same rigorous standards as your savings account. This is the vision driving the European bank consortium.

How This Compares to the US Approach

While Europe tightened its grip, the United States took a different path. In July 2025, President Trump signed the GENIUS Act (Guiding and Establishing National Innovation for U.S. Stablecoins Act). This legislation also mandates reserve requirements and redemption rights, mirroring MiCA’s core protections. However, the implementation timeline and enforcement mechanisms are notably more flexible.

The U.S. approach designates compliant stablecoins as "payment stablecoins," treating them similarly to electronic money but allowing for a broader range of reserve assets and slower phased compliance. This leniency has led analysts to predict a potential arbitrage opportunity. Traders and businesses might prefer operating through U.S.-based entities to access a wider array of stablecoins, potentially shifting transaction volumes away from stricter EU markets. Major players like Visa and Mastercard are already integrating these U.S. compliant stablecoins, further accelerating adoption outside Europe.

For a user in Wellington or Warsaw, this divergence means your geographic location increasingly determines your access to global crypto liquidity. The EU prioritizes safety and sovereignty; the US prioritizes speed and market leadership. Both models have trade-offs.

What Should You Do Now?

If you are currently holding non-compliant stablecoins like USDT in an EU-based exchange, your options are limited. First, check if your provider offers a conversion feature to a compliant asset. Many CASPs introduced temporary bridges to help users move from USDT to compliant EMTs or fiat euros. Second, consider moving your assets to a self-custody wallet if you wish to retain exposure, though remember you lose the ease of trading them on regulated platforms.

For new entrants, stick to tokens that explicitly state MiCA compliance. Look for issuers that publish monthly reserve attestations and offer direct redemption portals. As the European bank consortium launches its product later this year, keep an eye on announcements from major banks. Early access programs may offer better rates or lower fees for initial adopters.

The regulatory dust is settling, but the landscape is far from static. With the BIS warning about systemic risks and the SEC pushing its own "Project Crypto" strategy, expect continued evolution. Staying informed isn’t just good practice; it’s essential for protecting your capital in a rapidly maturing market.

Can I still buy USDT in the EU?

You generally cannot buy or sell USDT on regulated European exchanges (CASPs) as of Q1 2025 due to MiCA delisting rules. However, you may still be able to acquire it through decentralized exchanges (DEXs) or peer-to-peer networks, though these methods carry higher risks and lack consumer protections.

Is my USDT safe if I hold it in a private wallet?

Yes, owning USDT is not illegal in the EU. MiCA restricts trading services provided by licensed companies, not personal possession. If you hold USDT in a self-custody wallet, you retain control of your assets. However, you may face difficulties converting it back to fiat or other cryptocurrencies through regulated channels.

What is the difference between an EMT and an ART?

An E-Money Token (EMT) is pegged to a single fiat currency (like the Euro) and has simpler reserve requirements. An Asset-Referenced Token (ART) references a basket of currencies or assets, making it more complex and subject to stricter regulatory oversight similar to securities.

When will the European bank consortium stablecoin launch?

The consortium, comprising banks like ING and UniCredit, aims to launch its MiCA-compliant euro stablecoin in the second half of 2026. It is currently undergoing licensing processes with the Dutch Central Bank.

How does MiCA compare to the US GENIUS Act?

Both regulations require robust reserves and redemption rights. However, MiCA is stricter on reserve composition and enforcement timelines, while the US GENIUS Act offers more flexibility and faster implementation paths, potentially making the US market more attractive for certain stablecoin issuers.